A looming global food crisis: What should the global response be?

Unpacking the Four “Cs” of 2022 - Climate, Conflict, Covid and (high food) Costs

by Alexander Müller and Adam Prakash

Published on Apr 07, 2022

This post is a draft working paper for discussion, it will be further revised and adapted for publication.

Key Messages

We’ve been here before: The 2008 global food crisis showed us what the “perfect storm” that precipitates a global food crisis looks like.

We can expect much worse to come: The convergence of the Russian invasion and its disruption of agrifood supply chains, hyper inflation due to demand from economies recovering from the Covid-19 pandemic, high energy costs, record-high fertiliser prices, and rising demand for biofuels all indicate that a major food crisis is imminent.

A business as usual response is unthinkable: Having set out the evidence of a food, humanitarian, energy, climate, and economic crisis that is spiralling out of control, this article argues that complacency is not an option anymore.

What must world leaders do?

The convergence of the 4Cs demonstrates that the world has not learnt the lessons of the last major food price crisis in 2007-8. While urgent measures are needed to manage the unfolding crisis, we cannot afford to postpone the much-needed transformation towards more inclusive and climate-resilient economic systems.

Our analysis highlights four fundamental actions that must be put in place without delay:

Frame short-term policy responses within an overarching governance framework that seeks to transform our unequal and unsustainable economic systems.

Ramp up social protection measures for the most vulnerable and food-insecure populations.

Implement the global commitment to the progressive realisation of the right to food, adopted by members of the Food and Agriculture Organisation of the UN (FAO) in 2004.

Embark on a pre-emptive multilateral negotiation process to resolve the Ukraine crisis in the context of the 4 Cs to find systemic responses to these systemic (and increasingly global) challenges.

A gathering storm

The term “perfect storm” was widely coined to characterise the food (price) crisis of 2006-2008, when a confluence of negative events (successive poor cops, soaring biofuel demand, as well as an energy and financial crises) enveloped global food markets to send prices skyrocketing to record nominal levels. In June 2008, FAO FAO convened a World Food Summit in Rome that brought together around 60 heads of states and governments and more than 5,000 participants. Drawing lessons from the great world food crisis of the 1970s, in which millions of people perished, this constituted proof that the global food system is prone to vulnerable acute shocks that could reverberate around the world.

All signs point to the makings of another perfect storm in 2022. Thousands of people have already died and millions more displaced by the Russian invasion of Ukraine, placing greater Europe at the heart of an unfolding geopolitical crisis with global ramifications. While the full extent of the catastrophe is yet to be determined, the World Food Programme reports that the war in Ukraine is triggering a wave of collateral hunger across the globe as food and energy prices surge. Similar arguments were advanced in a recent New York Times article.

To understand the possible repercussions of these developments, it is necessary to analyse a range of possible scenarios, including a worst case scenario, in which hundreds of millions could experience severe hunger. This requires analysing the channels of vulnerability: the weaknesses and the risks embedded in the current global food system. At this point, its important to point out that the clouds were already gathering well before the onset of the war in Ukraine, as outlined in a recent Bloomberg report on why soaring prices for everything used to make food brings more inflation.

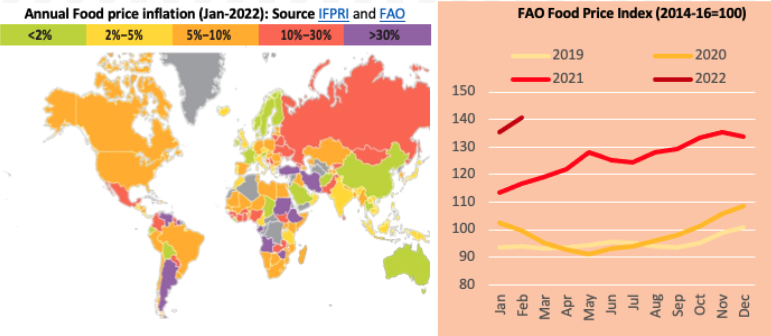

As shown in the visualisation of global food price inflation below, soaring demand coupled with scarce supply of goods and services leads to price hikes. The global spread of food price inflation is confirmed by the FAO’s Food Price Index (FFPI) – the global benchmark in measuring food price changes – which reached an all-time high in February 2022, and looks set to surpass the record again in March 2022.

Leaving aside an analysis of market fundamentals, it is broadly acknowledged that food insecurity co-exists with excess production and food waste. It is estimated that over the last decade, more than 800 million people on average have been left hungry despite there being enough food produced in the world to feed them. A holistic understanding of food security entails looking beyond food availability to examine the other three dimensions: access, utilisation and stability. Consequently, it is insufficient to measure food security through a supply lens only. A more instructive metric ought to take account of consumption patterns. Additional dynamics that determine food flows include the dominance of major food exporters in driving food demand and influencing the price of food, both in global as well as domestic markets.

Moreover, the world is rapidly moving on from the Covid-19 pandemic, exerting severe demand pressure on almost all globally traded commodities and their supply chains. This is particularly true for the energy sector, which, as explained below, has a direct impact on agricultural production.

Unpacking the big Cs

Conflict: Impact of the Russian invasion on global food supplies

From an international trade perspective, the role that both the Russian Federation and Ukraine in supplying the global arena is critical. Together, the two countries produce about 12 percent of the food calories consumed globally. Exports of food supplies are often concentrated in a handful of countries, exposing these markets to risks of and shocks and volatility, which can manifest in both supplies and prices.

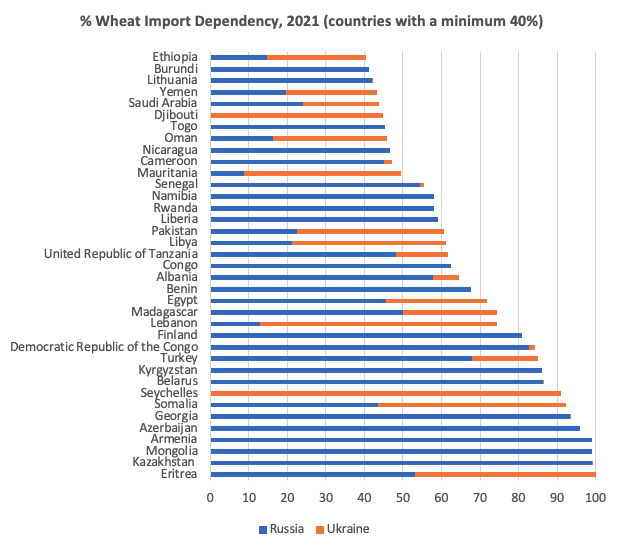

The following table illustrates the potential impact of disrupted supply chains on wheat importing countries.

Source: Trade Data Monitor

These ratios indicate a reason for alarm, especially for wheat. Even more so if Ukraine cannot harvest its crops owing to the conflict (wheat is expected to be harvested in July/August). If the country were to harvest its crops, Ukraine’s ports are set to stay closed until the Russian invasion ends. If Ukraine’s ports were to reopen, insurers, if willing to provide coverage, will demand high premia for vessels entering the Black Sea. Amidst ships being hit by missiles, war risk premia range in the hundreds of thousands of US dollars and have reached USD 300,000 for some vessels. Also, Russia may place export restrictions on its export crops or it may be faced with sanctions barring sales to the international marketplace. This means that there could be a combined 33 million tonne shock to the wheat market.

Source: Calculated from USDA data (accessed 19 March 2022)

Ukraine also stands out as a major oilseed supplier in the form of sunflower seed, which is typically crushed to produce vegetable oil. It is noteworthy that the price of vegetable oil globally, as depicted by the FAO Food Price Index, reached an all-time high owing to harvest uncertainties in Ukraine. This was further compounded by reduced availability of palm oil from in South East Asia in export markets, and a poor harvest of soybeans in Latin America.

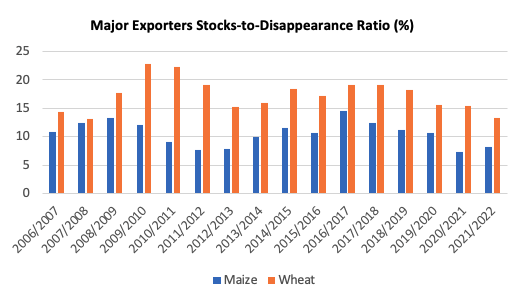

One of the most important market indicators of impending food crisis is the “stocks-to-disappearance” ratio of key commodity suppliers, which is simply the quotient of surpluses (stocks) over consumption plus exports. Analysis has shown that this ratio (or its expected equivalent) is a sufficient statistic in predicting food crises. As shown in the figure below, the ratio for wheat currently stands at 13 percent, the same level during the last food crisis of 2007/2008. This means that the major exporters can satisfy global needs for just 45 days. As for maize, the ratio is far lower, and is hovering at historical lows, providing a buffering capacity of a small window of 29 days. Even though maize has a number of coarse grain substitutes, and even non-grain feedstuffs, such as cassava, wheat is less substitutable.

Recent movements in international grain prices further reflect the current uncertainties in the global food system, as exemplified by benchmark export quotations for wheat, in which US No 2 Soft Red Winter Wheat increased by 52 percent between 21 February and 7 March this year.

A further troubling development for global food supplies is Russia’s dependence on imported pesticides and seeds. Pesticide use in the country is virtually instituted for the country's large-scale, input-intensive agricultural holdings. If the Russian Federation can no longer import these chemicals – which can potentially be used in chemical warfare – due to market sanctions, this could greatly affect the availability of many food crops, in domestic as well as international markets. This would further affect global food prices, and worsen food insecurity in import-dependent countries.

Costs of food production and supply

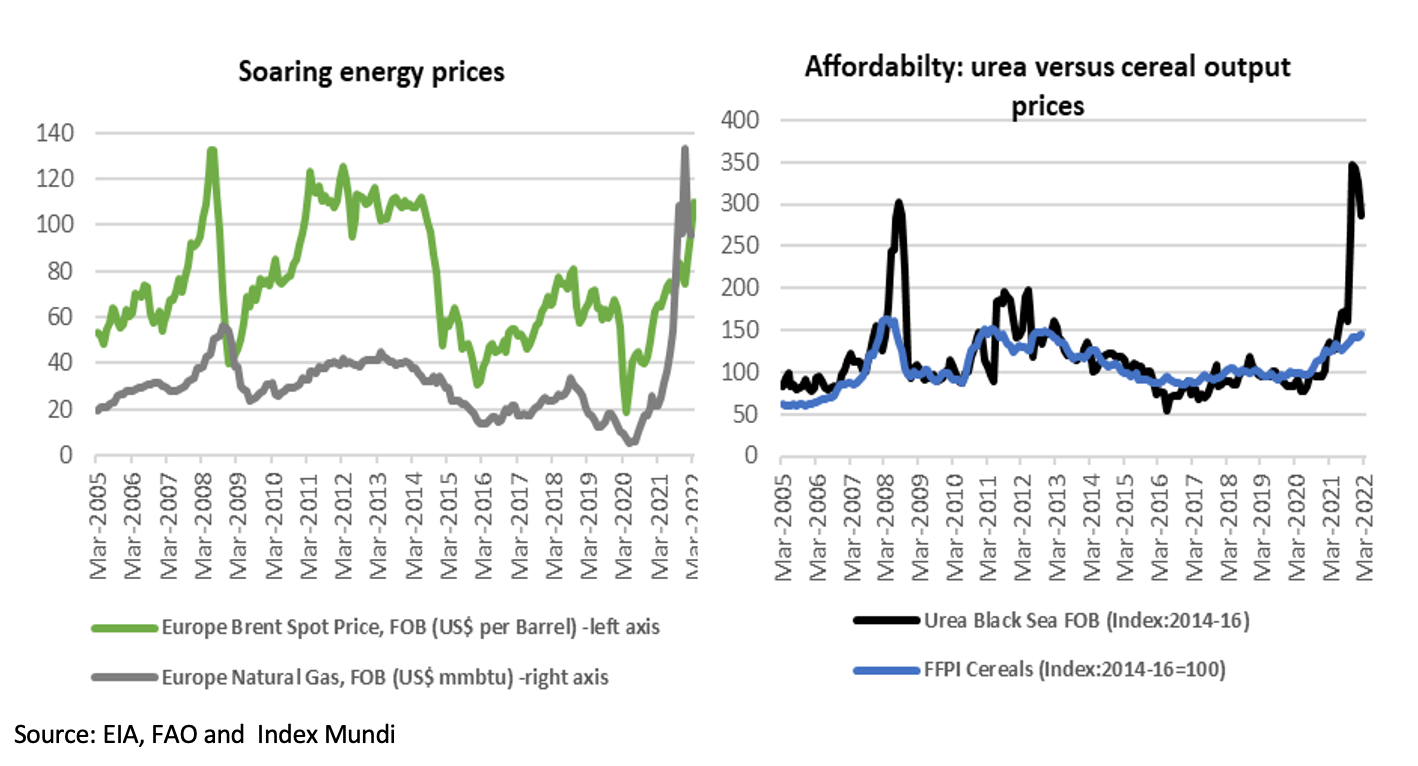

In addition to market supply constraints, rising fertiliser costs globally are greatly affecting commercial grain production. Nitrogen or N, in the form of urea, is the most critical ingredient for crop yields, and is typically made from natural gas and in some cases crude oil. Prices of these fossil fuels have reached unprecedented highs in recent months.

Record high fertiliser prices call to question the profitability of conventional intensive farming models. Beyond the farmgate, a recent study found that around three-fourths of the food costs to people worldwide are in the transport, processing, manufacturing and distribution of food, with fuel playing a significant role.

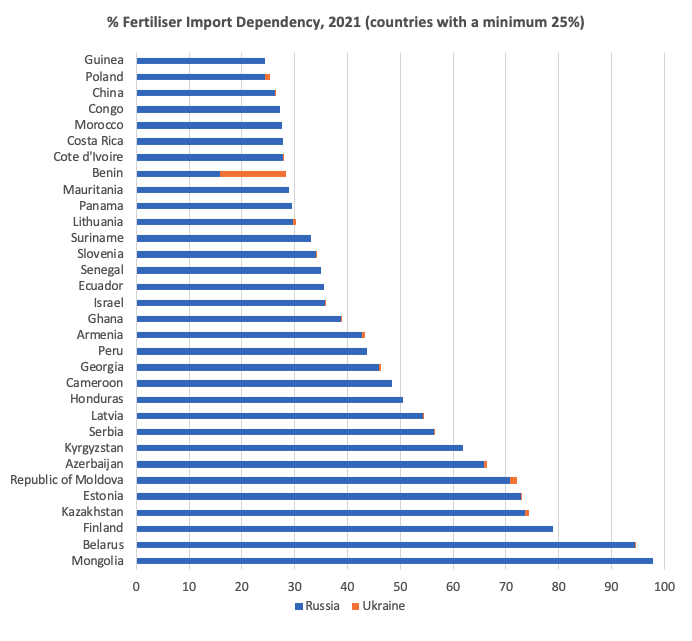

It is quite clear that affordability gap of urea vis-à-vis cereal prices has widened remarkably, even exceeding the unaffordability of the 2006-08 crisis. Ironically, Russia is the largest international supplier of urea and other fertilisers, with many countries located in the EU, Eastern Europe and Central Asia dependent on Russia for well over 50 percent of their fertiliser needs. Again, with the prospect of a trade embargo on Russia's exports, or self-imposed export restriction, the global fertiliser market would be subject to considerable disruption. As already alluded to, this prospect is already reflected in record urea (N) benchmark fertiliser quotations.

Source: Trade Data Monitor

Climate: Exploring some sustainability questions

Record prices for natural gas – the main source of N production – could open the door to more environmentally unsustainable sources of energy, that would be too expensive to explore under normal market conditions. One such option is the rise in fracking installations in the US.

Another option - as was the case in the 2006-2008 crisis – is an expected rise in demand for biofuels. With high crude oil prices, maize (the dominant ethanol feedstock alongside sugarcane) could increasingly be used for blended fuels, benefitting countries where discretionary blending already takes place. The current estimated demand for maize in animal feed market is estimated at 144 million. According to the USDA, an almost equal amount (135 million tonnes) of maize could be diverted to ethanol production in 2021/22.

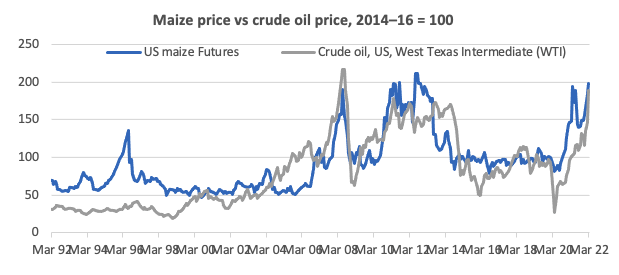

As fossil fuel prices remain on a sharp upward trajectory, the use of agricultural feedstocks for biofuel is shaped directly through energy prices. When crude oil prices rise there is a threshhold at which the production of biofuels from food crops - especially maize - becomes economically attractive. Hence, high energy prices encourage the conversion of larger quantities of agricultural feedstocks competitive for conversion into energy. Given the large size of the energy market relative to the food market, this pulls food prices up to their energy parity equivalent. It is for this reason that of agricultural energy feedstocks tend to correlate with crude oil prices as shown below.

Source: CME, EIA

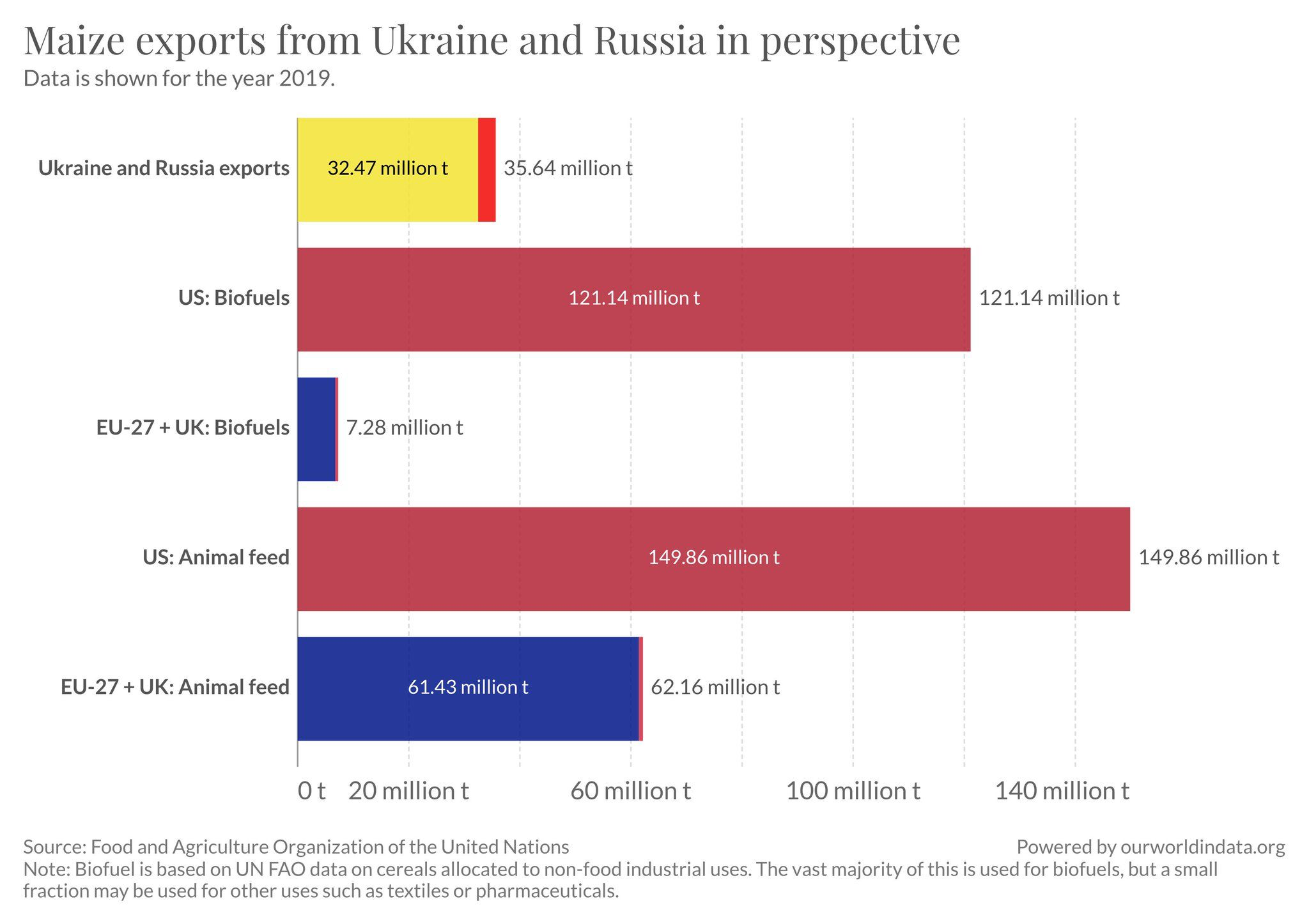

It is often “forgotten” that an enormous share of grain and oilseed crops produced are not used for direct human consumption but as animal feed. As an example, the United States and the EU are using a combined 211 million tonnes of maize as animal feed – 7 times the amount of maize exported from Russia and Ukraine in 2019. Together with around 130 million tonnes of maize used to produce biofuels in 2019, the United States and EU are diverting 341 million tonnes of production from direct human consumption.

Continued industrial production of meat casts a long shadow on the environment, incurring very high costs in terms of climate-destabilising greenhouse gas emissions, water pollution and a growing risk of antibiotic resistances as well as zoonotic diseases. Even from a human nutrition standpoint, it is necessary to significantly reduce meat consumption in industrialised countries. Consequently an immediate answer to any global food crisis is very simple: Feed people first!

All the fertiliser in the world, the best seeds and the most effective pesticides do not guarantee an effectual supply response. For there is one overarching variable that is more important in shaping productivity outcomes - the weather. If the world expands plantings in the hope of increasing exportable supplies, we will still be at the behest of the climate. Colloquially put, “the world needs good luck” such is the randomness of the weather in a world ever-confronting a climate crisis. And the prospects are not good. The 6th IPCC reported stated in no uncertain terms that if global warming increases, some compound extreme events with low likelihood in past … will become more frequent, and there will be a higher likelihood that events with increased intensities, durations and/or spatial extents unprecedented in the observational record will occur (high confidence).

In addition, NASA warns that climate change could make the situation worse if agricultural production in the world’s other breadbaskets is disrupted this year by extreme weather events.

The prospect of more extreme weather events (droughts, heat stress and floods) does not bode well for the global food system. No hemisphere, no continent and no country can be guaranteed to escape the increasing vagaries of the weather under a changing climate. This only compounds current uncertainties on the degree and extent of any prospective and protracted food crisis.

Exploring policy response options

In theory, the best way to alleviate crises is to let markets do their work. High food prices should send a powerful signal for farmers to expand plantings (i.e., a marked supply response). And – again in theory – it is expected that major exporting countries should refrain from restricting trade, either though bans or taxes. In an ideal world, with greater policy cohesion and market transparency, a self-amplifying crisis can be avoided by a combination of supply responses and guaranteeing the free flow of trade.

Given the convergence of the 4Cs, however, it is unrealistic to expect a “perfect” market response. Instead, we are likely to see a repeat of reactionary trade polices that fuelled the 2006-08 crisis. This could be aggravated by additional supply constraints due to the impact of the Ukraine conflict on spring wheat and maize in the northern hemisphere. While this could be counterbalanced by expected bumper harvests for major southern hemisphere exporters such as Argentina and Brazil, these countries expect well-below harvests for oilseeds. Furthermore, a La Niña Advisory has been issued for southern continents for the new season, which could spell poor prospects given prevailing drought conditions.

Moreover, a rising global population requires will place additional pressure on agricultural production. This raises the issue of how to accelerate the transition towards more climate-resilient agricultural production. Yara – a leading commercial global supplier of fertilisers – has predicted that if fertiliser is not added to the soil, crops can be reduced by 50 percent by the next harvest owing to yield reductions. While it is in the company’s interest to produce synthetic fertilisers, it does highlight the current lock-in of intensive production models. Can farmers afford (not) to apply fertilisers? Or could steep production costs lead to increased investments in bio-fertilisers and other less toxic alternatives?

Against this complex interplay of factors, what are the main considerations that policy makers should take into account?

A business-as-usual response will not work. History shows that reiterating the usual calls for countries to keep markets open and desist from piling up stocks will is insufficient to tackle the scale of the current food price and supply crisis.

A coordinated policy response is urgently needed to put the food needs of people first. This will require agreements for minimising the diversion of food crops(and land) to biofuel production and animal feed.

These immediate responses must be framed within an overall vision of creating a more equitable global food system. Transforming our unsustainable agricultural systems requires facing some hard truths. Current intensive livestock production systems demand huge amounts of land, water, and other vital natural resources. Moreoever, the overconsumption of meat in industrialised countries, as well as by elites in low-income countries – directly contributes to negative impacts on human health and the environment. Tough decisions will need to be made to reallocate available resources to safeguard food security for all.

Global agricultural sectors need to decouple themselves from environmentally harmful fossil fuel-based and – often – subsidised inputs. With these chemical-based inputs at or nearing record highs, an opportunity is presented to explore existing alternatives. Given the importance of nitrogen to crops, bio-fertilisers and the application of oilcakes are well established and so are crop rotation techniques using legumes for nitrogen fixation, noting that higher legume production could also satisfy dietary protein requirements at the expense of unsustainable meat, egg and dairy production. Bio-pesticides and integrated pest management (IPM) techniques have also long been established. These alternatives need to be placed at the top of the agreed-upon sustainability agenda of the United Nations.

Concerted action is also needed on the demand side. Efforts to reduce post-harvest losses and minimise food waste can contribute to food security improvements, and lessen pressure on the environment. It can also enhance the efficiency of the global food system and by shortening supply chains and reducing the costs of delivering food to the most vulnerable groups.

Social protection schemes for the poorest and most vulnerable groups are necessary to tackle hunger and famine. Cash transfers and related systems such as the Brazilian Programme “Zero Hunger” have proven their worth. Implementing the “right to food” as agreed by all FAO member states in 2004 is not only an effective way to avoid hunger in times of crisis but also an important safeguard to secure the transformation towards sustainable food systems, which do not impact the poorest.

To sum up, the 4Cs demonstrate that we have arrived at a defining moment. After Climate, Conflict and Covid, we now have to cope with high Costs. Our globalised food system is highly vulnerable to shocks, but has not put in place effective management structures to deal with increasingly complex challenges. Already, we are witnessing a rising tide of hungry and undernourished people, increasing the chances that a full-scale humanitarian crisis is underway. States and non-state actors must must act now to push the multilateral system to embark pre-emptive negotiations: this is critical to the holistic management of the 4Cs, and redirecting our economic systems towards planetary resilience and sustainability.

Extraordinary times calls for extraordinary interventions. Given its oversight role in the governance of international markets, the Agricultural Market Information System (AMIS) of the G20 is a critical actor in global food system governance. TMG calls on AMIS to make every effort to put the most exposed to food insecurity risks at the heart of their agenda. AMIS must address the four “Cs” in a holistic manner, promoting policy interventions to contain the trend in global hunger.

- Urban Food Futures Jul 27, 2026

Advancing Inclusive and Sustainable School Meal Programmes

TMG Research and its partners convened a stakeholder dialogue to launch a policy brief and facilitate dialogue on the design, financing and sustainability of inclusive school meal programmes, drawing on lessons from Mukuru.

Emmanuel Atamba, Cheboi Jerono

- Land Governance Jun 24, 2026

Women don't live in silos. The Rio Convention's Gender Actions Plans should match this reality.

Frederike Klümper, Judith Rosendahl (GIZ), Venge Nyirongo (UN-Women), Dr. Birguy Lamizana (UNCCD), Jes Weigelt

- Land Governance Jun 17, 2026

Beyond Decisions, Laws, and Regulations: Why Are Pastoral Areas Still Shrinking and Farmer-Herder Conflicts Rising?

This World Day to Combat Desertification and Drought, we ask why pastoral land in Niger continues to shrink despite decades of legal protection, and what it will take for the commitments made under the UNCCD to actually hold.

Kader Baba

Written by Alexander Müller and Adam Prakash